June 2025

December 2024

June 2024

March 2024

December 2023

September 2023

June 2023

March 2023

December 2022

September 2022

Property Fund

Quarterly Reports

June 2025

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the June 2025 half.

There has been a lot of activity to report. We have new valuations across our portfolio, all of which are significantly increased since the end of the 2024 financial year, but notably, none of which have relied on reduced capitalisation rates despite the 50 basis points of cash rate cuts, and 75 basis points of cuts being priced in by markets throughout the rest of 2025. The reason for this is that sales activity has been low while vendors and buyers wait out the RBA’s cuts, so there are no comparable sales that would inform a reduced capitalisation rate. So, while we only feel capitalisation rates are an appropriate valuation methodology for our O’Brien Street property, the guidance from the valuer is that capitalisation rates will be markedly lower for the end of the 2026 financial year, which will flow through to higher valuations.

To our new acquisition on O’Brien Street, Bondi Beach, our new tenant has recently finished the planned renovation and has commenced trading. Additionally, July marks the first month of rent, which will be roughly $220k per annum after outgoings. Versus our purchase price of $2.9m, the bank valuation came in at $4.1m, towards the low end of our expectation, but a 41% increase on our purchase price. Notably, the bank valuation accounted for the six-month rent-free period, so we anticipate another significant valuation jump next financial year.

Onto Avoca Street, Randwick, and our new valuation came in at a 5.9% increase on the prior year. Our view remains that this site is more appropriately valued as a development opportunity, especially with pending rezoning changes. The site has double frontage and a huge 295sqm land size. Notably, the rezoning continues to progress, and the latest guidance on the council website is that changes will be finalised by the end of this calendar year. The changes would mean an increase in the FSR (floor space ratio) from 2:1 to 2.5:1, an increase of 25%. If the timeline holds, we will explore acquiring a DA (development application) for the site, with the aim of marketing/selling the site with an approved DA.

Finally, the behind-the-scenes progression of our Campbell Parade site continues. The owner in the building we have been negotiating with continues to make progress, having recently bought another unit and getting his ducks in a row to reach 75% support. Our 33% voting rights remain critical to his development plans, and we are currently negotiating a sale with a delayed settlement.

Additionally, we have extended Boost Juice’s lease to $125k per annum and another five years, up from $80k per annum when we exchanged on the property (an increase of 56.25%). We are completing negotiations with Birichina Café, which has agreed to an increase to $100k per annum, up from $72k when we exchanged on the property (an uplift of 38.9%). Finally, Ikaria restaurant has reached out to extend its lease, and we have commenced negotiations.

The valuation on Campbell Parade has come in $1m higher than the prior year to $15.25m, an increase of roughly 7%, but still well short of the range in which we are negotiating to sell.

Finally, we expect to have completed financials within the next 6-8 weeks, which will include an updated (and increased) unit price to account for the valuation increases across the portfolio.

– Shannon Rivkin

December 2024

– Shannon Rivkin

June 2024

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the June 2024 quarter.

It has been business as usual with the RWPT’s properties during the second quarter of the calendar year, with the portfolio fully leased and no leases expiring this year.

However, we have begun negotiating an extension to the Boost Juice lease in Bondi Beach after the tenant reached out to negotiate terms, and we are currently discussing a significant increase to the current rent. Additionally, with a market review due on the Little Real Estate lease and a significant increase required in the annual rent, Little Real Estate has opted to let its lease lapse. This is important for our blue-sky development plans for the site, with the lease being the only one not containing a development clause. We will now begin a campaign to find a new tenant on a higher lease, and importantly, any new lease will include a development clause.

Further to our update for the first quarter of 2024, the behind-the-scenes discussions have ramped up significantly. In that update, we mentioned the discussions with an owner in the building who has an ambition to develop the site. Since then, our position has changed, and we now wish to act as the kingmaker for any development and open up a sales process to the broader market. The properties are not officially on the market, and there will not likely be a public marketing campaign as a first course of action. The politics within the building are a good reason to keep our intentions private for now. However, we have multiple real estate agents reaching out to deep-pocketed developers.

Within the quarter, we have had some very encouraging discussions, and there is no shortage of interest in the asset. Most buyers, for now, have expressed the desire to either buy the whole building or to buy an option from the fund while it approaches other owners in the building. One such formal offer included an option exercise price of $20m for the fund’s lots (versus the $15.7m purchase price and last bank valuation of $14.5m, which is used for the unit price), an offer that was rejected. Our view remains that as an amalgamated site, our lots are worth in excess of $20m and that if we are to retain some risk (as we would in only selling an option), we will need an offer at a higher price.

With levies remaining a sore point for owners – the AGM was held last month to approve strata levies for the next year, and it was a fiery affair – there is no rush, and we wish to move in a measured fashion. The desire from marooned owners to sell is only likely to grow over time, so it will ultimately come down to partnering with the right buyer. We continue to believe that the owner in the building, who wishes to develop himself, is the most logical buyer due to his relationships and confidence in amalgamating the site.

Remaining in Bondi Beach, the RWPT exchanged on a new acquisition in O’Brien Street. The site is a ground-floor commercial property with a liquor licence (with an existing restaurant fit-out), and we bought it for $2.9m (equivalent to roughly $22k per square metre rate). Our sourcing agent partner has already commenced discussions with a potential tenant, with the plan to split the site into two separate tenancies, quoting roughly $140k per annum (inclusive of outgoings) per tenancy. Our view is that this site is worth closer to $4m, so we’re very excited that we were able to secure such a quality asset in what remains a seller’s market.

Onto our Randwick asset, and there are no updates to report on with proposed zoning changes still moving slowly through the process.

As a final point of business, we are due to pay the annual payment of $0.05 per share within the next couple of weeks, which will accompany the release of the annual financial statements. As we continue to use the bank valuations to formulate the unit price, the unit price remains well below what we believe the underlying assets are worth. The tax returns have now been completed, with a new unit price of $0.81739 per unit. We wish to remind investors that they can opt to reinvest the distribution at the prevailing unit price. If you would like to action this or are unsure whether you are due to receive the distribution in cash or new units, please contact Sean Darwell by either email ([email protected]) or phone (0450792151). Financial statements will be sent out separately to this update.

– Shannon Rivkin

March 2024

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the March 2024 quarter.

While it was business as usual during the first quarter of the calendar year, with the fund fully leased and no lease extensions signed throughout the quarter, there has been a lot going on behind the scenes with the trust’s investment in Bondi Beach. Specifically, negotiations have continued to advance with an owner in the building about a development of the building. He is a key player in any potential development with his relationship with other owners in the building, and he is a very successful property developer in his own right.

When we bought into the building, and the 30+% voting power in the owner’s corporation that came with the purchase, our view was that we would be the kingmaker in any plans to develop. As one of the oldest buildings on Campbell Parade, the ongoing maintenance costs are very high (and likely to remain so) and should act as a catalyst to convince lot owners to sell. Additionally, rents and sale prices continue to soar in Bondi Beach, with some incredible comparable activity of late. There is a major development underway only several doors up on the same block (https://mayfairbondibeach.com.au/), and the early off-the-plan sales activity is very encouraging, with expected per square metre rates exceeding $100k. While a more detailed feasibility study is needed, the preliminary feasibility provided (with both conservative and bullish estimates) is very promising.

Since our purchase, the plan was to get our ducks lined up in a row while we waited for the right opportunity, and we hope we have now come to that time. The weighted average lease expiry for the five lots we own in the building is short, and any extensions have (and will) include development clauses. Our potential partner in development believes that now is the time to approach residential owners after a recent lot was unable to sell, most likely in our view because of the high strata levies. An early proposal of a structure has been submitted which we feel is a good starting point, and our hope is that we can negotiate a deal which properly rewards investors in the trust. Specifically, we intend on housing any development in a new fund, and there would be an effective sale of this asset into this new fund.

Onto the trust’s property in Randwick, and we continue to wait for zoning changes to be approved in Randwick council. The new tenant is trading well, although the rent is low as we’ve wanted to maintain our flexibility. Our leasing partners at Metro Commercial are going to begin offering the property to buyers looking for development sites, with an asking price of $7m (versus our purchase price of $5m).

– Shannon Rivkin

December 2023

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the December 2023 quarter.

While typically there isn’t likely to be much to report quarter-on-quarter (especially as the entire property portfolio is fully leased without any near-term lease expiries), there are a few noteworthy items to discuss since our last update.

While the main rationale behind the Bondi Beach purchase (70 Campbell Parade) was the recognition that the rents were well below comparable market rents – as well as the expectation that Bondi Beach would continue to generate above-market rental growth – there was also a strategic angle. Our view has been that 70 Campbell Parade stands as the last remaining apartment building with development potential on Campbell Parade.

Additionally, we believe that the position is far superior to other recent developments such as The Pacific or Noah’s (still to be developed, but which was bought at a very high price from a price per square metre basis), with the shortest distance to the water and a favourable north-east frontage. Strata levies have been very high in recent years – a short-term negative from a cash flow perspective, but a positive as far as supporting the argument to develop the building – and we stand in the enviable position of having a 33% voting share of the owner’s corporation. With 75% support required to force reluctant sellers into a sale for development, we effectively have veto power over any future development of the most strategically located apartment building in Bondi Beach, arguably the premier residential destination in Sydney.

With that in mind, we have held some early-stage discussions with a property developer who happens to be an owner in the building. He has prepared a feasibility study for the development of the building and has proposed several paths that we could pursue. While these talks are preliminary in nature and there is no certainty that anything will transpire, there are some exciting options for us to explore. The simplest such option would be to sell for a ‘premium to what was paid’ (to quote the preliminary proposal), and such a figure would be subject to negotiation and also present a potential opportunity cost in forgoing our unique position in the building. There will undoubtedly be other property developers keen on the site, but finessing the support of enough owners within the building may take someone on the inside with a relationship with other owners, so we are excited to continue these discussions. We will update investors as and when there is anything more concrete to report.

The second item of note is that we have amended the information memorandum (IM) to allow the fund to invest any spare cash in higher-yielding cash-like alternatives to cash in the bank. The commercial property market, despite the dramatic increase in interest rates over the last couple of years, has very much remained a seller’s market, and we are not having much luck on any new opportunities of late. The fund has been investing spare cash into term deposits, but there are better options available with better liquidity and higher returns, so a change to the IM is required.

Please click here to view the notice of change and the updated IM.

– Shannon Rivkin

September 2023

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the September 2023 quarter.

We discussed in the last quarterly update the process for the financial reports for the 2023 financial year, with valuations needed across the portfolio. With two key leases signed after 30 June, the valuer recommended that these leases were material and that valuations should be conducted after they had been executed. Additionally, the valuer required extensive information from the strata manager in charge of 68-70 Campbell Parade, and the strata manager had to be threatened with a vote to remove them before they started to provide what was needed. All these underlying issues have been the cause of the delay of the completion of the financial returns, and we apologise that this has been completed beyond the 30 September deadline.

Despite the delay, the advice from the trust’s tax agent is that there will be, as expected, no income or capital gains recorded throughout FY23, so there is nothing required to be included in one’s tax returns (please click here for a letter provided from the trust’s tax agent). This has been anticipated with first rent being paid from November only, and the rent being insufficient to offset many of the upfront costs associated with setting up the trust and executing the trust’s two acquisitions. The returns are currently being audited and will be released to investors separate to this quarterly update.

While the financial reports will be sent to investors in a separate note, the key highlights to note are:

- The bank valuations don’t take into account value above and beyond a simple net income and passing capitalisation rate. Additionally, bank valuations are notoriously conservative and are typically used to underpin a mortgage provided by a bank.

- a) In the case of Randwick, the lease was signed for the purpose of flexibility and some short-term income while we await rezoning and future development. The rent does not justify the purchase price, but our view on future income once we have more floor space to rent is that it will be well above the current rent, and therefore justify a considerably higher valuation. The valuation for Randwick can be downloaded by clicking here.

- b) In the case of Bondi, one of the key reasons we bought the properties was because of the high potential that a developer would want to purchase the building. The building remains one of the oldest residential buildings on Campbell Parade and has become increasingly expensive to maintain. While the elevated maintenance expenses are a short-term pain, it is this issue which we also feel will compel lot owners (many of whom are investors and not owner-occupiers) to sell to a compelling offer. So, there are some negatives in the short-term (lower net income and higher strata fees impacting the valuation) offsetting the strategic importance of an old building with high maintenance costs. The valuation for Bondi can be downloaded by clicking here.

- We discussed with the valuer the reduced strata levies for Bondi now that major capital works are behind us, but ultimately the valuer stated that an average of recent years would be used. While this impacts the current valuation, any legitimate sale would be marketed on future net income (not historical). In the event of a sale to a developer, there would be no concern about strata fees and comparable recent sales to developers have been for rates per square metre significantly above our purchase price. It is worth noting that the valuer advised that the valuation would have been at roughly the same level as the purchase price if strata levies were unchanged from 2022 (as opposed to the five-year average used).

- On the final point about a potential sale to a developer, we have had some preliminary talks with the other owner of the commercial lots in the building after he expressed an interest in purchasing the building. More than 50% of voting power is held between this other owner and the Rivkin Wholesale Property Trust. Owners amounting to 75% of the owner’s corporation would need to approve any sale of the building, so we have a considerable seat at the table.

In summary, there haven’t been any surprises from the valuer. On the back of rapidly increasing interest rates, we anticipated conservative valuations and have had to absorb the one-off cost of stamp duty. Otherwise, the strategy is going to plan, and we remain confident in the future return profile for the portfolio.

– Shannon Rivkin

June 2023

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the June 2023 quarter.

As the June quarter marks the end of the financial year, there is a lot going on to report to investors.

The first item of note is the financial year distribution that will be distributed to investors shortly, with a commitment in the information memorandum (IM) for a minimum $0.05 per annum.

As predicted in the IM, income only started flowing into the trust from December 2022, so the first distribution will be mostly in the form of capital returns (which will be tax free for investors), with taxable distributions likely to come from the end of the 2024 financial year. As part of this process, new valuations are being sought for the trust’s property portfolio which will help determine the new unit price. For those investors reinvesting distributions, the issue price of the new units will be determined once the valuations are received.

Typically, we would have engaged valuers immediately following the end of the financial year, but we have agreed terms on new leases for one lot in Bondi Beach and for the Randwick asset. Both leases will have material impacts on the valuations, so we have held off until these are completed. In the case of the Bondi lot, this is an extension with a long-term tenant called Gelbison Pizzeria which has been a tenant for over thirty years. The uplift in rent is over 20% and we believe that the leases across the entire Bondi are under-market and offer significant income upside. It is also worth mentioning that we have received further inbound enquiries from developers about the trust’s potential interest in selling, and we are exploring these opportunities further and hope to provide updates in due course. It is notable that the owner of 58 Campbell Parade has had its development application approved by the Land and Environment Court, serving as precedent for any future development of 70 Campbell Parade.

The lease that has been negotiated at Randwick has been a long time coming, with the dilapidated nature of the property proving an impediment for potential tenants, not surprisingly. As we are planning on developing the site once council approves the expected rezoning changes, we have been seeking a flexible lease to provide some short-term income, and we have finally found the right tenant. While the headline rent isn’t all that impressive, the lease allows for the termination of the lease for development of the site, so we are very happy with the outcome.

You can find the IM by clicking here.

– Shannon Rivkin

March 2023

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the March 2023 quarter.

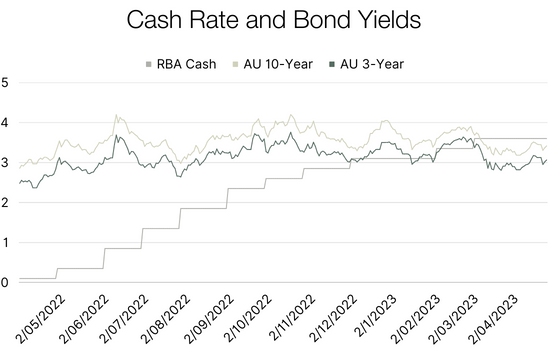

With the end of the financial year coming up, there isn’t a great deal to report to investors this quarter other than the changes in the macro environment which have been a big headwind for risk assets in 2022. 2023 has been a different story as inflation has started to roll over and the RBA has paused its rate rise cycle after ten straight months of increases. Most importantly, it is long-term rate expectations that have clearly peaked as demonstrated by the chart below. The importance of this change is supported by early signs that the residential housing market has bottomed.

Commercial and industrial property are sensitive to moves in cap rates (interest rates) and typically yield above the risk-free rate, with the margin being determined by the quality of the asset. Roughly 75% of the fund’s assets are in fully leased, beach frontage commercial property, and it is this type of asset that has continued to perform well in a difficult environment. Using the listed real estate investment trust (REIT) sector as a guide, and it is the assets that are seeing pressure on rents or on occupancy rates that are trading below net tangible asset backing (NTA) on the expectation that the value of those properties is held above their true value on respective balance sheets. Industrial property or high-quality shopping centres are trading at small discounts to NTA, whereas those names with big exposure to CBD office buildings are trading at significant discounts to NTA.

To the performance of the portfolio, and there isn’t much to report. The fund has spare cash and is looking to buy but price expectations, for the most part, have remained elevated for high-quality assets. With a full five months since the fund settled on its purchase in Bondi Beach, we are in early discussions with several tenants about extensions to their leases, with good comparable recent activity serving as a springboard to push for big increases. While the best result would be to extend the current tenants to avoid new leasing campaigns and incentives for new tenants, the previous leases are well below current market rates, and we expect a bumpy ride during these negotiations. In Randwick, we continue to seek out a short-term lease to generate some income while we await rezoning changes to be approved by the council but given the dilapidated state of the property and the desire for flexibility so that the site can be developed in the future, we remain selective on the lease we are willing to commit to.

Finally, the fund is preparing to pay its first distribution per the terms of the information memorandum (IM) by the end of the financial year. While the income in the fund won’t cover the amount of this first distribution (especially as we only started receiving rent in November after settlement), but this commitment was made to provide a consistent income. Additionally, we will engage external valuers to value the portfolio post 30 June, and we suggest reading the IM to get a good idea of what to expect. The net asset value (NAV) of the fund will include the cost of stamp duty as well, so the expectation is that the first NAV will be below the issue price, before rental increases start flowing in for next year’s NAV.

You can find the IM by clicking here.

– Shannon Rivkin

December 2022

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust (RWPT) for the December 2022 quarter.

Risk assets continued to fluctuate wildly throughout the December quarter, with continuing central bank hawkishness offset by softening economic and inflation data. Money markets continue to price in further rate increases this year, but also point to rates heading lower by the end of this year and early next year. With CPI-linked rents on the RWPT’s Bondi assets, we sit in the comfortable position of locking in higher income levels before asset prices start to head up once/if interest rates head lower. The likelihood is that property prices remain under pressure before beginning their recovery next year. It should be noted that we haven’t seen commercial property prices follow residential property lower, but lower activity makes a direct comparison imperfect.

Looking at the RWPT’s portfolio, the near-term upside for the Bondi assets comes from the expiry of existing leases. The property manager has been approached by several tenants about extending their leases well before lease expiry, but our view remains that the next leases are going to be on substantially increased per square metre rates, and we are contently waiting. Recent leasing activity on Campbell Parade are in some cases double the rates the old leases are on, so we expect the income profile to improve significantly over the next 1-2 years. Meanwhile, the property manager has begun engaging with some of the other owners about exploring some of the early-stage approaches from several property developers. While a sale is not a primary ambition in the short term, we mentioned in the last update that the strata have received several unsolicited offers in recent months, translating to a very attractive look-through value for our lots.

The Randwick asset has seen a few developments since the last quarterly update. The exciting news is that the council’s plans to rezone – which would increase the allowable height and floor space ratios (FSR) of the properties within the zone – have progressed, with the Randwick council having submitted the proposed changes to the NSW Department of Planning and Environment late last year. With this in mind, the game plan remains to find a short-term tenant (or a long-term tenant, but with a demolition clause in the lease), and discussions have advanced with one interested party. The point of the lease would be to provide some short-term income and allow us to borrow against the property, but the longer-term strategy remains a future redevelopment once the rezoning is approved.

You can find the IM by clicking here.

– Shannon Rivkin

September 2022

I am pleased to provide an update to investors in the Rivkin Wholesale Property Trust for the September 2022 quarter.

At a macro level, risk assets continue to experience extreme volatility as the outlook for inflation and interest rates remains murky, but commercial property has been a relative outperformer. Our theory behind this strength is that high-quality commercial property tends to experience rental growth in line with inflation throughout all cycles, suggesting that this year’s strong inflation (and likely next year’s) will translate to higher permanent income. In contrast, long-term interest rates are expected to revert to lower-than-average levels once this inflationary period is in the rear-view mirror, so arguably, the outlook for high-quality commercial property is brighter than other risk assets. I stress the ‘high-quality’ aspect of that definition, as a potential recession or slowing economy will most certainly impact the ability to lease lower-quality commercial property.

If that theory proves accurate, then our bullishness on our acquisition in Bondi Beach should pan out as demand for beachfront property continues to demonstrate resilience despite the weak macro conditions. One of the drivers of our purchase was that recent rental trends on Campbell Parade demonstrated how low the existing rents were on the properties we were buying. To put that view in perspective, two shops on 156 Campbell Parade were leased last month at a rate of $2,700 per square metre, whereas the average per square metre rent we will be receiving is roughly half that rate. With a short weighted average lease expiry (WALE), we expect a significant above-inflation increase in rents over the short and long term.

Another angle behind our purchase in Bondi Beach was the potential development upside of the building. While this is not a primary ambition in the short term, it is worth disclosing that the strata have received several unsolicited offers in recent months, translating to a very attractive look-through value for our lots. As we will settle our purchase on 1 November, we have been unable to explore these approaches, but we will look into this further in the coming months.

There is less to discuss with our Randwick property. We anticipated a long leasing campaign with the amount of work needed on the property, but we are encouraged by the early interest and remain optimistic about leasing the property on favourable terms within our original expected timeframe. There have been some positive developments regarding the potential rezoning that was rumoured when we bought the property, with the council releasing a draft Local Environmental Plan, which, if implemented, would increase the allowable height and floor space ratios (FSR) of the properties within the zone. This would be a huge win, and we will update investors as this process progresses.

You can find the IM by clicking here.

– Shannon Rivkin